October 3, 2022

Posted by Macquarie Asset Management

Market volatility and dislocation may create opportunities

Global real estate markets performed solidly in the face of elevated financial volatility in the first half of this year. Nonetheless, market downturns are a regular part of the business cycle and occur on average every seven years. While challenging, they are temporary and often provide opportunities, including in the commercial real estate sector.

We expect high quality buildings and property assets in stronger locations where there are supply-demand imbalances to continue performing solidly in this environment. Widening discounts for secondary assets and buildings with leasing risk or elevated capex requirements should create repositioning and repurposing opportunities, particularly in and around large urban markets and good locations.

Interesting opportunities also appear to have opened in public markets where implied cap rates have increased sharply relative to underlying private market values. This includes sectors with solid inflationary protection characteristics such as rental housing.

Other cyclical opportunities may include debt and equity investments in developers and assets that are most exposed to economic cycles and higher construction and financing costs, including in the residential sector. Softening housing markets may also create opportunities to acquire development sites and land in less competitive processes and at lower prices.

Looking beyond any near-term adjustment, pricing is likely to start firming again ahead of the peak slowdown in global growth and real estate fundamentals as investors take advantage of cheaper entry points, as we have seen in previous cycles.

Looking for a peak in policy rates

Faced with a sharp downturn, and huge uncertainties, policymakers implemented a historically large fiscal and monetary stimulus over 2020-21. The demand stimulus combined with supply disruptions contributed to a surge in inflation rates which have risen to their highest levels since the early 1980s in key developed markets.

This has caught central banks (ex-China and Japan) behind their usual tightening curve, and they are now aggressively normalising interest rates. While the aim is for a soft landing, where demand cools to match reduced supply, the risk of overtightening remains high, where unemployment rises sharply.

Until inflation is well contained, central banks are likely to tighten policy further, though at a slower pace if rates are already close to neutral levels. This tightening narrative is set to become more balanced over the next 6-12 months, particularly if labour markets deteriorate and businesses scale back spending plans.

Forward looking markets are already betting that rates will peak at lower levels than mid-year expectations. 10-year bond yields – which are key inputs for commercial real estate pricing metrics – have fallen back since mid-June peaks, partly because long-term expectations for inflation have eased.

Of course, the concern here is that policymakers blink in the face of elevated volatility without controlling price pressures first, which would increase the likelihood of a slower growth and higher inflationary environment, leading to weaker asset performance over the next decade.

Debt and demographics headwinds

Over the longer-term, slowing growth in global working age populations and elevated public and private sector debts are likely to reassert themselves as key constraints on long-term rates. As these demand and spending drivers become more influential, weighing on global growth, the structural decline in interest rates since the early 1980s is set to re-establish itself beyond any further policy tightening.

Importantly, following any near-term softening of valuations, downward pressure on risk free rates is likely to boost capital flows into private markets, supporting cap rates and real estate pricing over the longer term.

Strong investment markets in 1H22

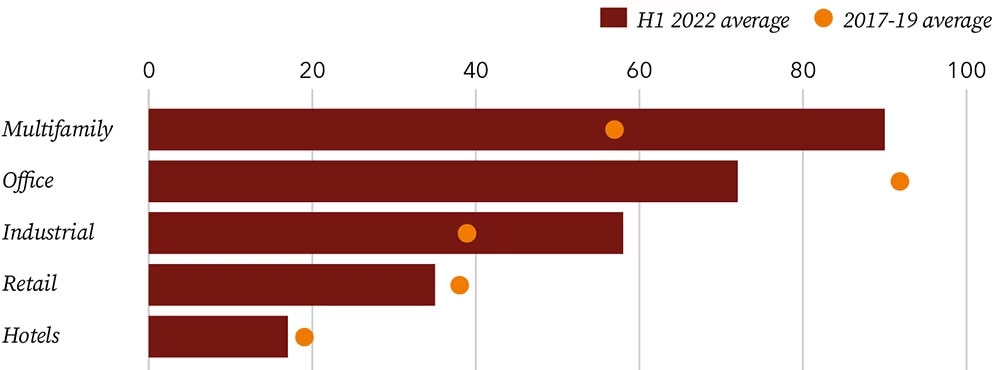

The global real estate market performed strongly in the first half of this year with transactions totalling close to USD 600 billion on a seasonally adjusted basis. Investments over the first half of the year were more than 20% higher than pre-pandemic averages. The uplift was broadly driven by higher prices, with the number of deals closed in line with 2017-2019 averages.

Industrial and apartments continued to drive activity, representing more than 50% of global investment. In other sectors, transactions recovered further, though activity was still below pre-covid levels, ranging from -10% for retail and hotels to -20% for offices.

Chart 1: Quarterly global investment volumes by sector (1H22 vs. 2017-2019 average, includes portfolio and entity sales but excludes sales of developments and land)

Source: MAM Real Estate

Strong investment activity and demand for real estate exposure supported pricing in 1H22 with NCREIF’s Open-End Diversified Core Equity (ODCE) index, a broad benchmark for US private markets, posting a 12% levered total return.

Transactional momentum may have peaked

Looking ahead, softening global growth is likely to temper near term investment activity. Highly levered borrowers and public market Real Estate Investment Trusts (REITs) that are trading at sizeable discounts to underlying asset values are likely to be less active for the remainder of this year. More restrictive public and private debt markets may also contribute to slower activity.

However, investors with long term strategies and strong relationships with traditional lenders are expected to continue to deploy capital, particularly in more resilient sectors, markets, and cities. Moreover, any further recovery in equity markets and falling bond rates are likely to improve the ‘denominator’ impact of allocations to private markets, allowing institutional investors and other multi-asset allocators to resume their normal investment flows into real estate.

Other investors with large cash piles and dry powder are also well positioned to take advantage of any pricing dislocation, usually with more equity than originally planned. These deals can then be refinanced at better terms as and when debt markets become more accommodative to boost returns.

In the absence of a sharp acceleration in near term growth though, the twelve-month investment total to 2Q22 may well be the peak in global transactions in this cycle. The upswing is likely to be linked to expectations of the next synchronised rate cutting cycle, as it has been previously.

Pricing against fixed income alternatives

Over the past decade, commercial real estate yields have exceeded those of fixed income alternatives. Elevated risk premia have supported capital inflows and investment activity into private real estate. Yields on 10-year government and investment grade corporate bonds have been depressed by the expansionary activities of central banks, which has increased the relative strength of real estate yields and supported cap rate compression.

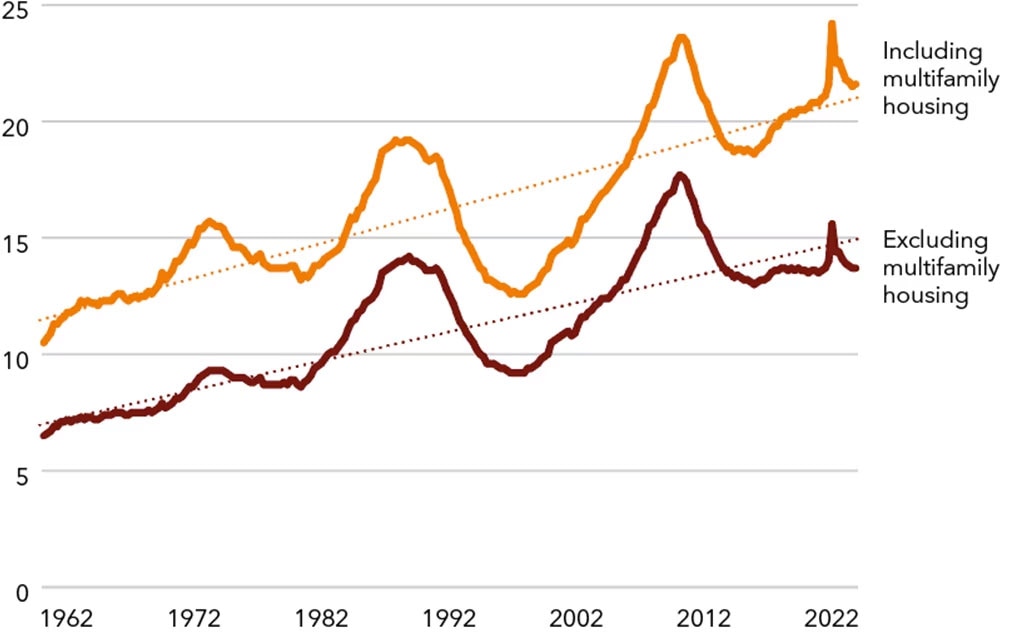

Real estate investors, developers and lenders have also been more cautious in their use of leverage over the past decade relative to previous upswings, at least in aggregate. This is reflected in the total outstanding debt secured against US commercial property, normalised by nominal GDP.

Chart 2: US outstanding debt secured against commercial and multifamily properties

Source: MAM Real Estate

The sharp rise in credit relative to GDP in the lead up to both the early-90s recession and Global Financial Crisis (GFC) amplified real estate’s volatility as lower valuations led to tighter credit conditions which, in turn, further impacted pricing. Outstanding US credit today including rental housing is now in line with historical trend levels (and most likely well below in the case of Europe) and unlikely to exacerbate sector volatility in a mild recession.

Searching for pricing visibility

However, given the sharp bond market selloff in the first half of this year, commercial real estate yields are now tight relative to fixed income alternatives, though spreads remain positive and above previous cyclical lows in the case of sectors such as prime CBD offices.

Private real estate has been able to absorb the rates shock via lower risk premium spreads, which is reflected in the stability of valuation yields and broker estimates on pricing. Of course, these tend to lag and reflect pricing on deals from several months earlier.

If bond yields continue to move lower from mid-year peaks, for example, if global growth continues to slow, spreads between cap rates and bonds may normalise further. However, part of the pricing adjustment may also need to come from higher property yields, if, as expected, required returns have reset in line with higher risk-free rates and increased macro volatility and financing costs this year.

Green Street’s marked-to-market indices which are based on transactions that are currently being negotiated and contracted have already recorded slight capital declines of -5% from recent peaks and more for secondary buildings and non-core locations in Europe and the US.

Housing markets exposed to higher mortgage rates

Broad pressure on owner occupier housing markets where prices are softening in the most levered markets such as Australia, Canada, and New Zealand may also weigh on household spending, though residential prices remain firm at a national level in the US and UK, for now.

Public market rental housing owners appear to have been caught up in this broader housing slowdown where higher mortgage rates are impacting sales and revenues of home builders. Whereas underlying revenues of rental housing providers are supported by stretched affordability for potential home buyers and positive household formation rates as pandemic disruptions ease, including gradual normalisation of international migration.

Rental housing’s strong rental growth and short-term leases – allowing owners to capture inflation uplifts quickly – underpin the sector’s resilience through cycles. Unwinding of pandemic stimulus payments to households and rising unemployment may help dampen rental growth over the medium term, ensuring rental affordability remains in check for tenants.

In Europe, regulated caps on rental growth may also explain the selloff of rental housing in public markets – particularly in Germany – given cashflows cannot be reset in line with annual inflation rates as they can be in Australia, US, and UK.

Construction costs and development activity

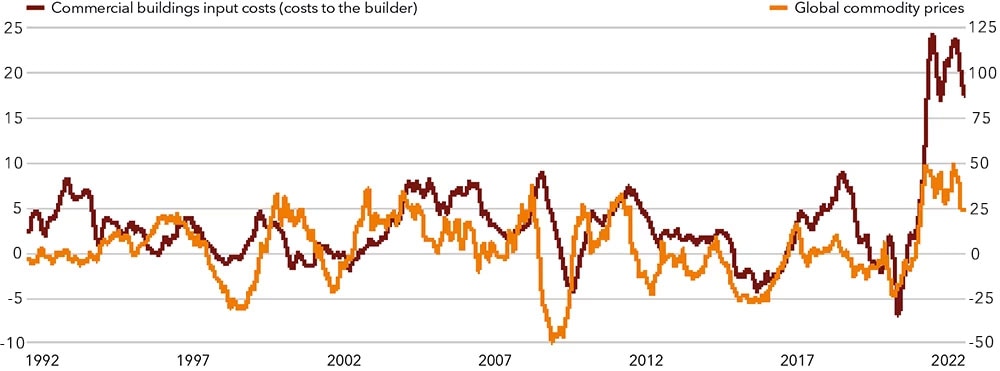

In the pre-COVID world, build costs and tender prices in developed markets rose in line with CPI inflation, at around 2-3% per annum. Over the past 12 months, construction costs have jumped sharply around the world, driven by a surge in global commodity prices. Costs have also been pushed higher by a general shortage of workers and higher wages.

Cost inflation appears close to peaking though, and should fall back over the medium term, particularly if raw material prices slide further with weaker global growth. However, the shift back to pre-covid averages may be hampered by ongoing tight labour markets, particularly in the absence of a mild recession.

Development margins have been maintained in markets and sectors with strong demand drivers and rental growth. This includes the logistics sector in locations around major metros and key ports with tight vacancy rates, where higher construction costs can be passed onto tenants via higher rents.

In other sectors and markets, if land prices remain firm, higher construction costs may help to balance future demand-supply dynamics as development pipelines are pared back given tighter yield-on-cost metrics. This should help to protect values of existing buildings or at least provide a floor for pricing.

Chart 3: Global commodity prices and US commercial building input costs

Source: MAM Real Estate

Focused real estate strategies

Elevated macro volatility tends to increase focus on fundamentals and income growth profiles across sectors, markets, and product types. Overall, we think that higher quality buildings and assets in stronger locations where there are supply-demand imbalances and landlords can pass on cost pressures to tenants are expected to perform better, including under a mild global recession.

Rental growth and cashflows are likely to remain relatively strong for industrial and rental housing supported by tight vacancy rates and those institutionalising sectors that are less exposed to economic growth such as data centres, though total returns are likely to be lower than in recent years if cap rates soften from current lows.

In the office sector, the polarisation between prime and secondary demand is set to become more pronounced as corporates look to minimise costs, including shedding non-core and underutilised space. Larger discounts for secondary assets are expected to create repositioning and repurposing opportunities.

Underlying drivers of the movement to high quality space include the growing importance of technology in the workplace and shift to hybrid working models, desire to attract and retain talent, and rising ESG considerations as tenants and investors shift towards their long-term net zero targets.

[3139275]

This article was first published by PERE in October 2022 and is reproduced here with permission.

Before acting on any information, you should consider the appropriateness of it having regard to your particular objectives, financial situation and needs and seek advice. No information set out above constitutes advice (including legal, tax, accounting or investment advice)

Nothing presented should be construed as a recommendation to purchase or sell any security or follow any investment technique or strategy.