A conversation with Kommunal Landspensjonskasse | February 2022

March 14, 2022

Posted by Macquarie Asset Management

The UN Climate Change Conference (COP26) last November in Glasgow has focused minds on the scale of the challenge ahead if we are to transform our society and economy to achieve the decarbonisation goals outlined by the Paris Agreement. With the investment community to play a key role in mobilising the finance needed to accelerate the low carbon transition, we invited Kommunal Landspensjonskasse’s (KLP) Chief Financial Officer Aage Schaanning and chief climate change advisor Lars Erik Mangset to discuss with Macquarie Asset Management’s Co-Head of Private Credit Tim Humphrey how investors can help finance the fight against climate change.

Investing sustainably has risen up the agenda for institutional investors globally, with environmental considerations and decarbonisation increasingly influential when shaping investment strategies. How have these themes influenced KLP’s approach to investing?

Aage Schaanning (AS): KLP has been around for a long time, having been established in 1949. As a mutual company, we are owned by Norwegian municipalities and health enterprises, and we expect one million people, around 20 per cent of Norway’s population, to receive a KLP pension in the future. We manage €80 billion within the fund today, with half of our assets invested in Norway.

At the top of our agenda, is, of course, trying to achieve a good return. But as Norway’s largest pension fund we also recognise that we have a responsibility to the savers and communities we represent. That is why we are focused on making our investments contribute to the low carbon transition. We want to make sure that what we do, across all asset classes, is aligned with the goals of the Paris Agreement.

Most energy production in Norway tends to be clean hydropower, so we have a long history of investing in the renewable energy sector locally. In recent years though we have expanded this clean energy investing into other markets, including emerging economies.

In 2014, we also established exclusion mechanisms for coal, tar, and sand, which have become more stringent over time. Our approach has been to reallocate capital from these carbon-intensive sectors to the renewable energy sector so that we can help to accelerate the low-carbon transition.

Lars Erik Mangset (LEM): We have set ourselves a target to invest a minimum of €600 million each year in climate-friendly projects. But in addition to investing in renewable energy, we have also set net zero targets for our entire investment portfolio.

When setting our net zero targets, we need to analyse each company within our portfolio of more than 8,000 companies. With a very broad and diversified portfolio such as ours, this is not a straightforward process, so we are currently developing our framework to make this commitment operational.

We know there will be substantial challenges, especially in accessing complete and consistent data. However, the key point is that we must focus on the continuous improvement of our Paris-aligned investment framework to meet our ultimate decarbonisation objectives.

How have managers responded to the growing appetite of institutional investors such as KLP to finance the low-carbon transition?

Tim Humphrey(TH): The desire of investors to have an impact on this important investment theme has seen considerable capital committed in recent years to strategies which invest equity in green energy projects. However, we have also seen growth on the debt side of the equation, with institutional investors able to carve out a large and growing space in the private, green energy debt market.

Source: Macquarie Asset Management analysis of IJGlobal infrastructure database (January 2021)

Opportunities in green energy debt are often sourced through bilateral negotiations or with a small club of lenders. It is much more akin to the types of lending banks historically did but have been less able to do with longer-dated projects recently due to changing capital requirements. Often, these opportunities are in a loan format, so they do not have external ratings, nor are they traded on a public exchange.

Macquarie Asset Management was an early mover in this space, with our private credit team making its first green energy debt investments in 2014. We have made more than €2.6 billion of investments across 38 green energy projects globally in solar plants, rooftop solar, onshore and offshore wind, and bioenergy since then. Much of this has been through our infrastructure debt-focused funds and mandates but the scale of the market, and strong engagement with the asset class from leading institutions such as KLP, has justified the need for dedicated strategies which address the opportunity.

Source: Macquarie Asset Management internal database (September 2021)

What is driving interest in green energy debt?

AS: We have very long-dated liabilities, so bonds or loans with a long duration are an ideal match for us. The long-term nature of green energy debt makes the asset class very attractive from an asset-liability matching point of view. Of course, the risk/return must be satisfactory, which is also achieved, especially because of the illiquidity premium that green energy debt offers. We are in a position where we can give up liquidity and benefit from that premium over a longer time frame.

TH: The illiquidity premium is a key differentiator for many investors. Green energy debt is not traded on public markets and is less liquid than many other asset classes. That poses a risk to some, but it also can be an opportunity for investors with a very long-term investment horizon such as KLP.

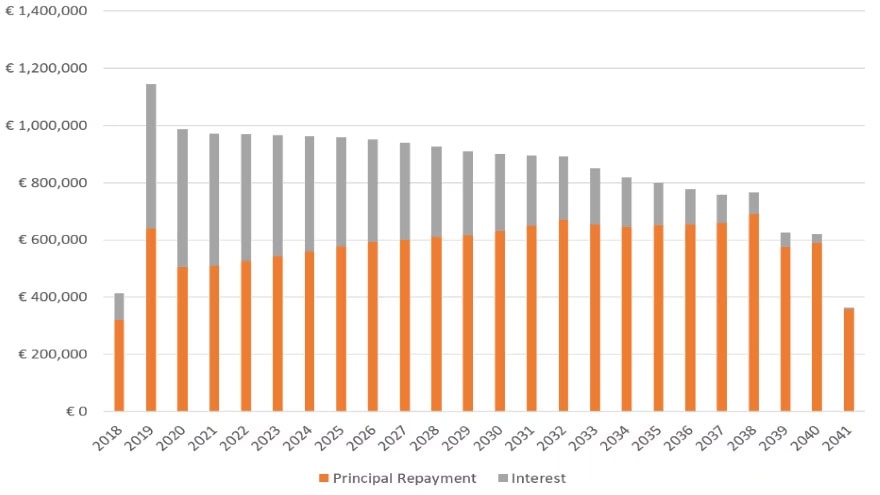

It is also possible to structure investments with relatively predictable revenues to ultimately deliver a stable debt cash flow to the end investor at a risk/return profile comparable to corporate bonds. This allows these investments to go into the corporate bond or fixed income allocation of many of our clients’ portfolios, particularly those portfolios that are focused on liability-matching or that are heavily regulated and need high-quality investments.

Example of cash flow profile

Source: Macquarie Asset Management internal analysis

So green energy debt can offer a potential yield enhancement for a fixed income portfolio but, equally as important at the moment, additional diversification. There is a lot of corporate credit risk and GDP correlation often running through portfolios, and these characteristics of green energy debt can potentially deliver diversification away from some of those risks.

With many investors looking to the asset class to support their net zero goals, how can investors ensure they are making a measurable and meaningful contribution to the fight against climate change?

TH: There are understandable concerns within the broader investment landscape about greenwashing as managers seek to capitalise on growing interest in sustainable investment strategies. One of the great things about green energy debt is that you are often directly investing in a project where you can see exactly how funds are used. This enables investors to credibly measure the impact their money is having at the end of the day.

LEM: Having a strong green claim in a structure or platform is extremely important for us. Especially given our net-zero goal, there needs to be clarity and credibility around investments that we end up labeling as “green”. We need to ensure these investments are making a direct contribution to the goals of the Paris Agreement.

I think the merits of having direct investments into sectors that are aligned with the EU’s taxonomy for sustainable activities also gives strong support to the claim that these assets are having an impact on achieving net zero. Not only this year, but for many years to come.

What is the scale of the opportunity?

TH: Over the next three decades, we expect to see more than $US8 trillion invested across both solar and wind projects globally. A substantial proportion of this investment is likely to come from debt investors, so someone has got to plug that funding gap. There are deep pools of capital within the private markets which can be utilised to do this.

AS: I completely agree. We must take urgent action this decade if we are to adapt our economy and society to slow the effects of climate change. Transitioning to cleaner energy must be central to this work.

The investment needed to do this will be significant, and institutional investors such as us must step up to the challenge by financing these projects with our long-term, stable capital. The opportunity is significant, and green energy debt can offer a win for both the climate and investors too.

[3137894]

IMPORTANT RISK CONSIDERATIONS

This market commentary has been prepared for general informational purposes by Macquarie Asset Management (MAM), the asset management business of Macquarie Group (Macquarie) and is not a product of the Macquarie Research Department. This market commentary reflects the views of speakers and or the related MAM investment team and statements in it may differ from the views of others in MAM or of other Macquarie divisions or groups, including Macquarie Research. This market commentary has not been prepared to comply with requirements designed to promote the independence of investment research and is accordingly not subject to any prohibition on dealing ahead of the dissemination of investment research.

Nothing in this market commentary shall be construed as a solicitation to buy or sell any security or other product, or to engage in or refrain from engaging in any transaction. Macquarie conducts a global full-service, integrated investment banking, asset management, and brokerage business. Macquarie may do, and seek to do, business with any of the companies covered in this market commentary. Macquarie has investment banking and other business relationships with a significant number of companies, which may include companies that are discussed in this commentary and may have positions in financial instruments or other financial interests in the subject matter of this market commentary. As a result, investors should be aware that Macquarie may have a conflict of interest that could affect the objectivity of this market commentary. In preparing this market commentary, we did not take into account the investment objectives, financial situation or needs of any particular client. You should not make an investment decision on the basis of this market commentary. Before making an investment decision you need to consider, with or without the assistance of an adviser, whether the investment is appropriate in light of your particular investment needs, objectives and financial circumstances.

Macquarie salespeople, traders and other professionals may provide oral or written market commentary, analysis, trading strategies or research products to Macquarie’s clients that reflect opinions which are different from or contrary to the opinions expressed in this market commentary. Macquarie’s asset management business (including MAM), principal trading desks and investing businesses may make investment decisions that are inconsistent with the views expressed in this commentary. There are risks involved in investing. The price of securities and other financial products can and does fluctuate, and an individual security or financial product may even become valueless. International investors are reminded of the additional risks inherent in international investments, such as currency fluctuations and international or local financial, market, economic, tax or regulatory conditions, which may adversely affect the value of the investment. This market commentary is based on information obtained from sources believed to be reliable, but we do not make any representation or warranty that it is accurate, complete or up to date. We accept no obligation to correct or update the information or opinions in this market commentary. Opinions, information, and data in this market commentary are as of the date indicated on the cover and subject to change without notice. No member of the Macquarie Group accepts any liability whatsoever for any direct, indirect, consequential or other loss arising from any use of this market commentary and/or further communication in relation to this market commentary. Some of the data in this market commentary may be sourced from information and materials published by government or industry bodies or agencies, however this market commentary is neither endorsed or certified by any such bodies or agencies. This market commentary does not constitute legal, tax accounting or investment advice. Recipients should independently evaluate any specific investment in consultation with their legal, tax, accounting, and investment advisors. Past performance is not indicative of future results.

This market commentary may include forward-looking statements, forecasts, estimates, projections, opinions and investment theses, which may be identified by the use of terminology such as “anticipate”, “believe”, “estimate”, “expect”, “intend”, “may”, “can”, “plan”, “will”, “would”, “should”, “seek”, “project”, “continue”, “target” and similar expressions. No representation is made or will be made that any forward-looking statements will be achieved or will prove to be correct or that any assumptions on which such statements may be based are reasonable. A number of factors could cause actual future results and operations to vary materially and adversely from the forwardlooking statements. Qualitative statements regarding political, regulatory, market and economic environments and opportunities are based on the related MAM team’s opinion, belief and judgment.

Investing involves risk, including the possible loss of principal.

Past performance does not guarantee future results

Diversification may not protect against market risk. Investment strategies that hold securities issued by companies principally engaged in the infrastructure industry have greater exposure to the potential adverse economic, regulatory, political, and other changes affecting such entities.

Infrastructure companies are subject risks including increased costs associated with capital construction programs and environmental regulations, surplus capacity, increased competition, availability of fuel at reasonable prices, energy conservation policies, difficulty in raising capital, and increased susceptibility to terrorist acts or political actions.

Liquidity risk is the possibility that securities cannot be readily sold within seven days at approximately the price at which a fund has valued them.

None of the entities noted in this document is an authorized deposit-taking institution for the purposes of the Banking Act 1959 (Commonwealth of Australia). The obligations of these entities do not represent deposits or other liabilities of Macquarie Bank Limited ABN 46 008 583 542 (MBL). MBL does not guarantee or otherwise provide assurance in respect of the obligations of these entities.