Perspectives

26 May 2021

China now dominates the world’s market for private education, and it’s growing fast, driven in large part by the after-school tutoring (AST) sector - itself a multi-billion dollar industry that can barely keep pace with parental demand for top-up education.

Such demand is leading to intensifying competition as EdTech companies and traditional educators fighting for market dominance. Head of Consumer and Education of Macquarie Equities Research Asia, Linda Huang, says that the country’s smaller cities and regional areas have become the main battleground for AST providers. She also believes that a hybrid model of online merge offline (OMO) tutoring will eventually prevail.

“Macquarie research shows there are real opportunities for education providers to leverage technology and begin to capture market share in what is an established but still fast-growing market,” Huang says.

At Macquarie’s inaugural DELTAH China Conference, Macquarie’s Asia Equity Research team explored the barriers to entry and just how the fragmented, regional nature of the AST market presents unique opportunities for companies with the capital needed to both innovate and acquire a national following.

China’s higher education system is fiercely competitive. In their final year of high school, students take a national, standardised test known as the ‘Gaokao’, which largely determines which university they can enter.

In 2019, just 1.6 per cent of a total population of more than nine million students who sat the Gaokao were accepted by top tier universities, graduates of which can expect to earn an average 27 per cent more than their peers.1

But academic competition between Chinese students begins well before their final year of high school. Students also undergo rigorous state-administered testing in year nine (the Zhongkao) to determine whether they qualify for an academic senior high school or a vocational one.

In a country where education is one of the main keys to social mobility, Chinese parents are often willing to pay more on their children’s private tutoring to improve their performance in such public examinations. This has encouraged the development of the world’s leading market in after school tutoring (AST).

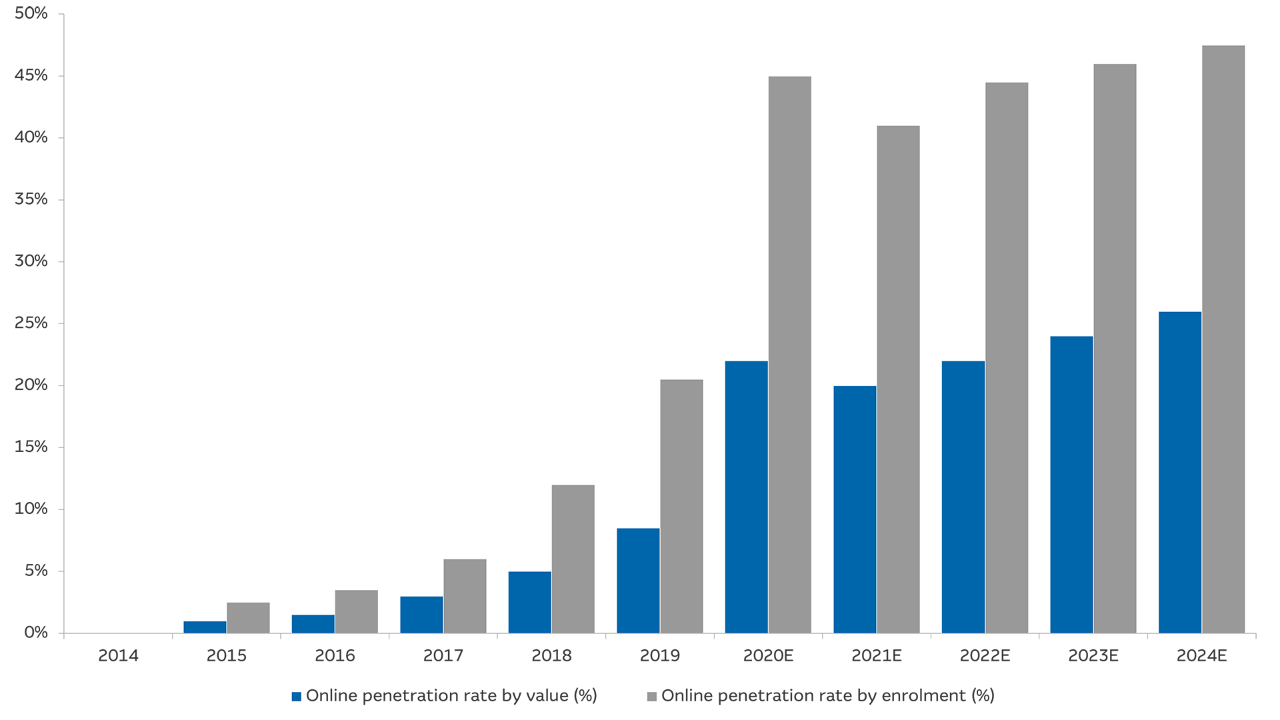

The Macquarie Proprietary Online Education Survey polled 10,000 Chinese parents from tier one to five cities. It found that as China’s education system becomes more competitive and the population becomes more affluent, AST is becoming more popular than ever before. In 2019, some 325.3 million students were enrolled in AST. By 2023, we expect this to rise to 659.5 million students, representing a CAGR of 19.3 per cent.

We also forecast that the market will grow by 89.5 per cent - from RMB619.1 billion ($US96.14 billion) to RMB1,173.1 billion ($US182.17 billion) - over the same period.

Source: F&S, Macquarie Research, January 2021

Traditionally, most tutoring has happened face-to-face in large centres, but this has been changing recently, Huang explains.

“Chinese students are already busy, so the idea of sitting in traffic for several hours to cross a city and attend a prestigious AST provider is not necessarily appealing,” she says. “The take up of online tutoring has been further accelerated by the COVID-19 pandemic.”

However, Huang believes that OMO’s hybrid approach to learning will become the most popular AST delivery model over the coming years as students supplement small in-person classes with online teaching.

“That way, students have access to leading teachers but also to one-on-one tutors who can make sure they solidify lessons and understand the subject matter,” Huang explains. “They also have the flexibility to move more towards online when they need to - such as during a lockdown.”

OMO is already proving particularly popular in China’s Tier 3 cities and regional areas, which account for more than half of the country’s 1.4 billion residents. No fewer than 71 per cent of Macquarie survey respondents opt for OMO as the preferred tutoring model, with 52 per cent saying that they would prioritise this form of learning for their children.

There are compelling reasons for its popularity among students in such areas. China prides itself on the egalitarian nature of its exam-based system. Theoretically, any student with high enough marks can enter the most prestigious universities such as Peking, Fudan or Tsinghua. However, the reality is that most students at the very top universities still come from Tier 1 and Tier 2 cities, where the best teachers, best-funded schools and most educated parents tend to congregate.

And yet, for all of AST’s popularity, it remains an incredibly fragmented market. More than three million companies are registered to provide AST in China, and the top two providers account for just 6.2 per cent of the nation’s market, although this has increased from 1.6 per cent five years ago.

While the online tutoring market is more concentrated, even here the top four players enjoy a combined 30 per cent market share.

One of the main barriers to capturing greater market share has traditionally been the cost of customer acquisition. By summer 2020, online players were spending more than RMB1,000 ($US155) to acquire every new student, an upfront expense smaller companies have found increasingly difficult to bear.

As a result, Huang believes the more significant players who have access to the capital they need for aggressive marketing and customer acquisition are the ones most likely to win.

“There is room for consolidation, and we expect to see some major players come to the fore over the next few years,” Huang explains. “While the cost of acquiring each new customer is relatively high, the customer relationship can be a long one - even stretching from a student’s primary school years through to university - so there is a payoff.”

“Our analysis shows that the lifetime value of a student could actually be more than RMB4,500 ($US700), which justifies the acquisition cost.”

Huang argues that brand recognition is another key to capturing market share in the sector. One way more cashed-up online ASTs can do this is by hiring high profile teachers who can provide a lesson for up to 10,000 students at the same time.

Huang also says some AST companies are using more innovative ways to become more embedded in China’s national psyche. For example, Youdao, a well-known educational app developer with an established base of followers, uses its popular portable dictionary pen to drive organic traffic to its OMO operations in a cost-effective way. The pen allows students to translate between traditional Chinese, simplified Chinese and English instantly.

Huang also believes market-leading AST, New Oriental Education & Technology Group, has a bright future in China’s OMO market. Although it is the country’s best-known face-to-face AST provider, it has been investing heavily in the online space too, including taking a 55.2 per cent stake in online provider Koolearn. Interestingly, Koolearn’s second-largest shareholder is tech giant Tencent, providing perhaps the ultimate platform for driving new customers.

“There is little doubt China’s vast AST system will move online, and we believe that OMO will be the preferred model. At the end of the day, the companies that prevail will be those that can scale most effectively.”

Learn more