Press Release

Sydney, 02 June 2010

Michael Evans’ article of Monday May 31, BusinessDay, P1, "Return of the boys with Brazil" relies on the premise that Macquarie raised money cheaply under the Australian government guarantee and deployed it, to "rebuild the bank and its bonuses".

This premise, and the article itself, are misleading in a number of ways:

Greg Ward

Chief Financial Officer

Macquarie Group

FURTHER DETAIL

CLAIM: Macquarie says CAF contributed 10 per cent of Macquarie's $1 billion net profit. Its operating revenue contribution appears to be significantly higher.

FACT: CAF contributed 6.8 per cent of Macquarie’s total operating income and a smaller percentage of net profit after tax. This can be easily calculated from the full year accounts which have been publicly disclosed.

CLAIM: At a time when the bank faced the collapse of its "Macquarie model" of fee-generating listed infrastructure trusts, Brazil began spearheading a drive to reinvent the bank's profitability using a turbocharged commercial lending strategy that taxpayers have unwittingly supported. The origins of CAF's rise lie at the height of the global financial crisis in September 2008.

FACT: All specialised funds - listed & unlisted infrastructure, real estate and private equity - provided only 12% of group operating income in 2007, 19% in 2008, 14% in 2009 and 10% in 2010. CAF has provided finance since 1970 and asset management solutions since mid 1990s to retail, corporate and government customers in 36 countries.

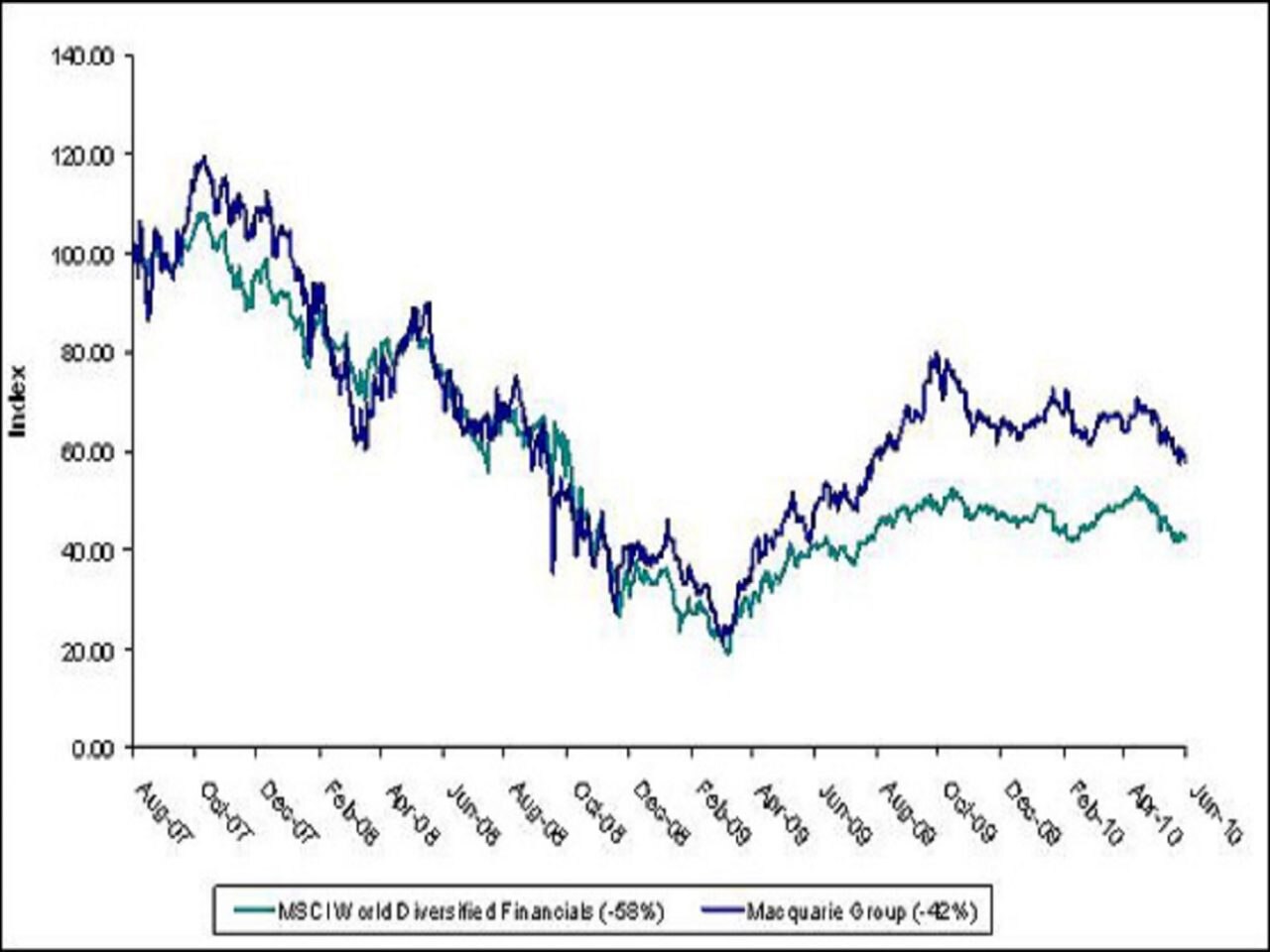

CLAIM: As BusinessDay revealed earlier this month, Macquarie undertook a lobbying effort with regulators and government as hedge funds mauled its share price, sparking a crisis of confidence.

FACT: Your article of 17 May 2010 “Revealed: MacBank’s code red to the government” did not reveal a lobbying effort by Macquarie; it only reported the subject line of a small number of email communications. With regard to the Macquarie Group share price since the start of the GFC, the movement in the Macquarie Group share price largely mirrored or outperformed the movement of share prices of financial institutions around the world as reflected in the MSCI World Diversified Financials Index. This is illustrated in the following chart:

CLAIM: Macquarie figured there was money to be made buying loan and leasing books below cost. … As borrowers still pay the same amount of interest on their loan, Macquarie's yield becomes much higher. … But Macquarie could also finance deals more cheaply and increase its margins even further. … There is also the potential for revaluing a rebound in the loan book's asset values as profit in the bank's profit-and-loss account.

FACT: In a period of market dislocation, Macquarie continued to provide finance to clients. This was a time when some foreign financial institutions either were not lending in or were withdrawing from the Australian market, including GMAC, which ceased originating retail and wholesale new business in Australia during 2008 and 2009. Macquarie was able to acquire these businesses and continue to support these customers.

CLAIM: Given the decision of experienced industry players to get out of the market, Macquarie's investment reveals the bank's ongoing strong appetite for risk - even if it is ultimately underwritten by the Australian taxpayer.

FACT: CAF operates under the stringent risk control framework it has always maintained and while its loan and asset book has increased, the quality of the book has remained consistent.

In general, Macquarie’s risk management principles have remained stable over 30 years and have served the organisation well over the course of the global financial crisis. Any suggestion Macquarie has a large appetite for risk is not supported by the facts, including the simple truth that Macquarie has remained profitable throughout its existence, including the recent market turmoil.

CLAIM: In a series of disclosures, Macquarie has detailed the rise of the CAF division, making limited commentary on its funding and profitability. / Macquarie places little emphasis on the effect of the business on the bank's overall profitability.

FACT: Macquarie provides extensive disclosures about all of its business divisions, CAF included, in annual reports (for Macquarie Group and Macquarie Bank), investor presentations, Management Discussion and Analysis and Pillar III filings. In addition, as noted elsewhere in the article, the head of CAF, presented at the Macquarie Operational Briefing in February this year, providing additional operational details about CAF which are not required to be disclosed. In addition, as part of the normal rotation of Macquarie’s business heads at operational briefings, the head of CAF also presented to the market in September 2006.

CLAIM: In the midst of the crisis CAF bought a multibillion-dollar plane- leasing book from financial crisis victim AIG, $1.8 billion in European loans and a $500 million US information technology leasing business.

FACT: It was in fact on 14 April 2010 – when financial markets were in recovery - that Macquarie agreed to acquire an aircraft operating lease portfolio from International Lease Finance Corporation (ILFC), a subsidiary of American International Group, Inc. (AIG).

Australia and New Zealand

T: +61 2 8232 2336

Email regional contact

Americas

T: +1 212 231 1310

Email regional contact

Asia

T: +852 3922 4772

Email regional contact

Europe, Middle East and Africa

T: +44 20 3037 4014

Email regional contact