Perspectives

20 May 2021

China is on the brink of a revolution when it comes to the way it moves food from cultivator to consumer. And as the largest global consumer of fresh produce per capita, all eyes are on those trying to bring the benefits of digitalisation to the country’s food supply chain.

Macquarie research estimates that hypermarkets, supermarkets and convenience stores hold a 37 per cent share of the country’s fresh produce market, coming in just below that of farmers’ and wet markets, which have the largest, at 38 per cent. Such an open market offers a massive opportunity – as well as and unique challenges – for those trying to capitalise on the growth in online food buying.

Like almost all countries, fresh food in China is one of the last retail segments to move to online channels, with internet purchasing accounting for just 5 per cent of total category sales1. The complexities of getting perishable produce from field to farm market require, however, a different skill set than for other retail products and long-life consumables.

With a complex supply chain structure, fragmented distribution network and constraints from cold-chain logistics capability, success in the space requires re-thinking logistics and delivery infrastructure. But, for those who meet the requirements for rapid scalability and reach the country’s mass population, the opportunity is enormous.

At Macquarie’s inaugural DELTAH China Conference, Macquarie’s Asia Equity Research team examined how online players are now leveraging capital and data to transform and expand foodservices distribution digitally.

“China’s food market is worth more than RMB5 trillion ($US77.4 trillion) a year. As it currently stands, online sales account for only around five per cent of that,” Han Joon Kim, Head of Internet and Media, Equity Research Asia at Macquarie Group, explains.

“The pandemic has drastically changed the way Chinese consumers buy and receive almost everything and fresh produce.”

China was a leader in online commerce before COVID-19, and the pandemic only further accelerated digital take-up. In the twelve months to August 2020, online retail jumped from 19.4 per cent to 24.6 per cent of total spend, according to UN data.2

This trend permeated all parts of China’s retail sector, including food sales. More importantly, online food buying is set to increase. One McKinsey survey found 55 per cent of Chinese consumers intended to continue buying more groceries online even after the pandemic.3

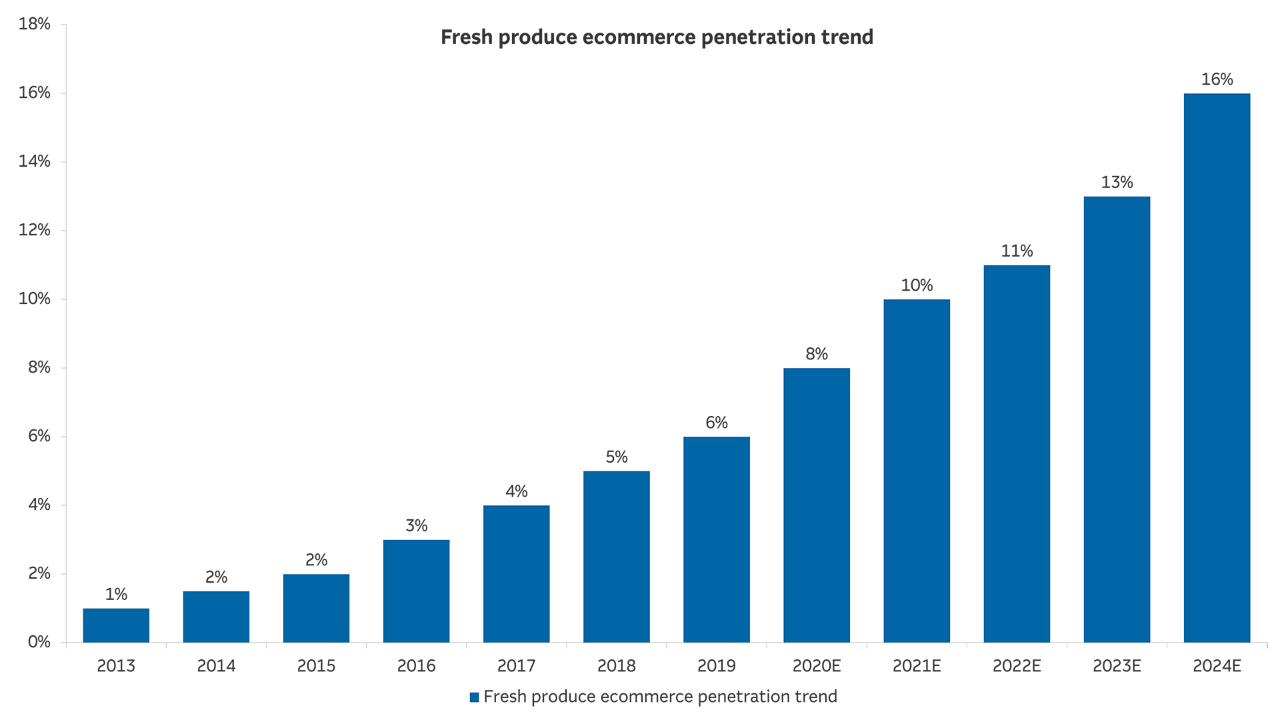

"The online penetration of the fresh food category should rise from 5 per cent in 2018 to 16 per cent by 2024. Though most of the Mainland China has largely recovered from the pandemic, many of the high-frequency consumers of online food have been sustained, and users are continuing to make regular online purchases."

Han Joon Kim

Head of Internet and Media

Equity Research Asia at Macquarie Group

Source: Euromonitor, Macquarie Research (October 2020)

“And unless Chinese food consumption habits change rapidly, future growth will increasingly depend on a very different model to facilitate the delivery of fresh food. It will also require a very significant investment in infrastructure to make it work,” he adds.

This could be good news for reducing the high level of food lost during storage, transport and processing; at around 35 million tonnes a year, it’s equal to roughly six per cent of all the food produced in China.4

Though digital retail heavyweights such as Alibaba, JCB and Pinduoduo – who together control around 80 per cent of China’s online retail spend – are in a strong position to disrupt the grocery market and gain online share, their existing approach is generally viewed as being most effective in Tier 1 cities – the country’s biggest.

Outside of those areas, ‘community group buying’ (CGB) has emerged as one of China’s most important digital trends.

CGB integrates small orders from households in the community into a large order. This model requires a central ‘community leader’ to negotiate with the supplier and coordinate the delivery and pickup from a central warehouse.

The aim is to largely disintermediate the expensive last mile of the delivery process by having consumers come out of homes to pick up the goods. This has made it particularly popular amongst price-conscientious consumers in Tier 2 and Tier 3 cities and spawned a $US11.5 billion industry.

Their success is, however, attracting the attention of the internet giants, which have begun investing in CGBs and implementing aggressive subsidy programs to recruit community coordinators and local suppliers.

Much of their focus has been on disintermediating the ‘last mile’ – the final step between distributor and consumer. However, so far, it has very much been a case of trial and error, even for these businesses. For instance, Alibaba’s ‘new retail’ initiative, launched in 2018, sought to bring 30-minute delivery to anyone living within a 3km radius of a Hema supermarket. The model proved to be unscalable, particularly in those smaller centres where CGB has taken off.

Kim says in 2021, most players are banking on a 6 to 18-hour delivery timeframe being acceptable to consumers. They are use a more multi-layered approach, where produce can be delivered to distribution centres or direct to the home, depending on the locality.

JD.com, another leading e-commerce player, has been investing in private player Xingsheng in a show of commitment towards the micro fulfilment grocery business model. Xingsheng’s group purchase platform operates in lower-tier cities in 14 Chinese provinces to help close the ‘last mile’ gap in the delivery network and serve neighbourhoods with fresh foods and daily necessities where online shopping is still in its infancy.

But Kim says that this is still early days even for the final mile and even more significant investment will ultimately be required further up the supply chain, especially in refrigeration.

In China, fresh food accounted for 90 per cent of the total tonnage of cold-chain logistics, with pharmaceuticals making up most of the rest.5 Pinduoduo, a leading online e-commerce asset-light business, has committed capital to build up cold chain logistics facilities.

“This will help reduce spoilage and bring down the cost, making online ordering both safer and more competitive. Improving the supply chain is the key to both fresher and more affordable goods,” Kim explains.

For those prepared to spend time building and perfecting their model, their rewards should ultimately be there.

“Increasing market share and capturing some of that spend is a once-in-a-decade opportunity,” he concludes.

“China’s produce market has a very different proposition from that of most other countries,” says Kim.

“In the United States, frozen products bought from the supermarket account for the most significant portion of the food market, and you have an established supply chain that has been built to facilitate this.”

In the United States, agriculture is undertaken by large scale producers who tend to supply to one organisation. The average farm in the US has 102 hectares of arable land; the average Chinese farm has just 1.6 hectares of arable land.

This means China’s path from field to dinner plate looks very different. Fruit and vegetables, as well as meat, are generally stored at room temperature. Produce must be sold and used quickly.

As a result, food is generally sourced from close to home, spoilage rates are high and food safety remains an issue.

Learn more