Perspectives

22 October 2021

A decade ago, the Australian Government commissioned its independent advisory body, the Productivity Commission, to review the provision of long-term care and support for people with a severe or profound disability.

The Commission found that the existing support system gave people with disability little choice and no certainty of access to appropriate supports. It highlighted how a systematic lack of independent, supported accommodation was not best serving the needs of individuals with significant care and support needs.

It found that as a result, an unacceptably high proportion of people had little to no choice outside of living in accommodation unsuitable for their significant care and support needs, including in residential aged care or nursing homes despite their young age, living at home with elderly parents, or in unsuitable public housing.

Image credit: Summer Housing

Image credit: Summer Housing

At the same time, the system was found to be 'underfunded, unfair, fragmented and inefficient', placing increasing cost pressure on public funds.1

To address these shortcomings, the establishment of a national, government-funded scheme for people with disability was recommended. The benefits of such an arrangement were noted as outweighing the costs and had the potential to add almost one per cent to Australia’s gross domestic product by 2050.2

The National Disability Insurance Scheme (NDIS) was established in 2013, centralising funding of long-term high-quality care and support for people with significant disabilities.3 For individuals with extreme functional impairment or very high support needs4 - approximately six per cent of NDIS-eligible individuals – this included the provision of high-quality, bespoke and community-integrated homes.

Importantly, the NDIS was structured to provide government payments directly to participants to empower them to make their own choices about their care and accommodation needs. This was a transition away from the traditional block-funding model and allowed the individual to directly fund specific services and providers.

To facilitate this new approach and establish a private sector-led market to fund, build and manage the new accommodation, Specialist Disability Accommodation (SDA) was introduced by the National Disability Insurance Agency (NDIA) - administrators of the NDIS - in 2016.

Once fully operational, it is forecast that annual government funding for SDA will reach $A700 million per annum5 to support eligible participants. Still, as an estimated $A10 - 12 billion market,6 private capital is required to build out the scheme.

The government provides an above-market rental stream to incentivise private market participation in the SDA sector7 and encourage investors to incur the upfront capital costs to develop accommodation to meet the needs of NDIS participants.

A range of private sector investors brings competition, and this incentivises providers to invest in their accommodation, offer housing in desirable geographic areas with access to services, and properly market residences to attract tenants. Private sector participation also ensures a competitive market that provides the highest standard of accommodation to meet the requirements and expectations of participants. Continued innovation and investment will be needed to remain competitive.

“The individual is driving the outcomes. The centrality of individual choice and control that is fundamental to the NDIS means that, in a competitive market, accommodation providers need to continually raise the bar with the best possible homes in the right location to attract tenants. The regulation and allotted pricing sets the parameters within which providers must operate,” says Ben Barry, Executive Director at Macquarie Asset Management.

Given the scale of the ongoing need for quality accommodation, an underlying government framework and regulatory regime, and some early participation from infrastructure investors, SDA is evolving from a nascent to an emerging institutional investment class. Creating a market that is driven by private investment has allowed SDA to attract capital from competitive debt markets and global equity investors. The regulatory framework creates a clear understanding of the revenue stream and what the NDIA perceives to be appropriate risk-adjusted returns.

“Investing in infrastructure brings with it an element of risk, and social infrastructure, such as this is no different. But in a world awash with investment opportunities, it’s important for attracting private capital that there’s clarity over the parameters in which operators are working and how that will impact customer demand for the product now and into the future,” says Barry.

Moving away from a block funding model to one that covers the full cost of ownership and operation of buildings means a larger universe of potential investors, including financiers, institutional investors and family offices, are able to be mobilised.

Macquarie has been engaged in the SDA sector since 2017, contributing to its growth towards becoming a stable asset class. Our involvement - with our housing partners, government and other market players - has helped raise awareness and understanding of SDA as an asset class.

“Both the deployment of our own balance sheet and our reputation as an infrastructure investor helped drive early momentum and have played an important role in developing this new sector,” says Barry.

Working directly with high-quality SDA providers – those who best understand the needs of SDA participants – Macquarie has directly enabled the creation of more than 230 SDA dwellings across Australia.

Not-for-profit organisations such as Summer Housing and Youngcare are working with Macquarie by assisting in dwelling design and procurement, marketing accommodation to prospective tenants, and helping to facilitate the provision of the services needed by the individual.

"We believe that by investing in, and coalescing partners around, the development of real assets that underpin society and communities we add real and lasting value for those who use and depend on them. This work closely aligns with our purpose: investing to deliver positive impact for everyone,” adds Barry.

With an initial focus on new build properties across Australia’s mainland cities, and which are located close to key infrastructure amenities, Macquarie expects to continue to grow its capability in the sector with the support of its clients.

Measuring the impact of SDA on the lives of individuals through numbers does not do it justice, but official data does show that it is having a positive effect.

Collectively, the number of specialist dwellings now stands at over 6,224 – including new build dwellings and dwellings that existed before SDA was implemented – which are supporting over 16,000 individuals across Australia. Providing people with who have the most significant care and support needs with access to this accommodation has seen the number of those under the age of 65 entering residential aged care fall by two thirds (68 per cent) since SDA launched.8

Source: National Disability Insurance Agency

The sector remains in its early stages, though, and has plenty of opportunity for growth and maturity ahead of it.

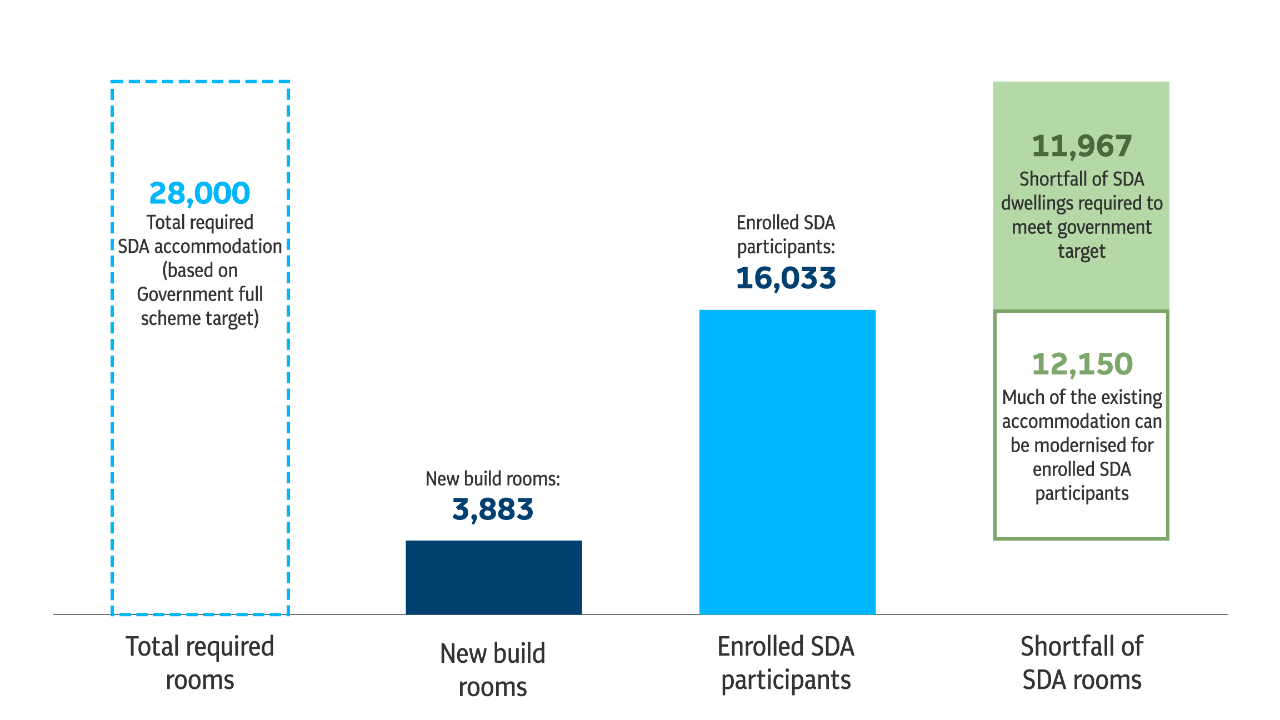

In the five years since the inception of SDA, just 3,883 new build places have been built, with the remainder of NDIS participants residing in existing disability housing stock - much of which no longer meets today’s standards.

On the optimistic assumption that construction levels increase to 2,000 rooms built a year, it will take another six years to close the current gap of around 12,000 places and meet the government target of 28,000 rooms.

Source: COAG Disability Reform Council, National Disability Insurance Scheme Quarterly Report, 30 June 2021

Source: COAG Disability Reform Council, National Disability Insurance Scheme Quarterly Report, 30 June 2021

‘Specialist Disability Accommodation Pricing and Payments Framework’, Australian Government, Department of Social Services, June 2020, https://www.dss.gov.au/

Andrew Beer, Kathleen Flanagan, Julia Verdouw et al., ‘Understanding Specialist Disability Accommodation funding’, Australian Housing and Urban Research Institute Limited, 21 March 2019, https://www.ahuri.edu.au/

‘National Disability Insurance Scheme (Specialist Disability Accommodation) Rules 2016’ (Cth), Australian Government, 27 March 2019, https://www.legislation.gov.au/

‘NDIS Specialist Disability Accommodation: Pathway to a mature market’, PWC and Summer Foundation, August 2017, https://www.summerfoundation.org.au/

‘Specialist Disability Accommodation: Market insights’, SGS Economics and Planning and Summer Foundation, 2018, https://www.summerfoundation.org.au/

1. ‘Disability Care and Support’, Productivity Commission, Report no. 54, 31 July 2011, https://www.pc.gov.au/

2. ‘Disability Care and Support’, Productivity Commission, Report no. 54, 31 July 2011, https://www.pc.gov.au/

3. ‘Disability Care and Support’, Productivity Commission, Report no. 54, 31 July 2011, https://www.pc.gov.au/

4. ‘Disability Care and Support’, Productivity Commission, Report no. 54, 31 July 2011, https://www.pc.gov.au/

5. ‘Governments take action to increase Specialist Disability Accommodation’, NDIS, 8 February 2019, https://www.ndis.gov.au/

6. ‘NDIS Specialist Disability Accommodation: Pathway to a mature market’, PWC and Summer Foundation, August 2017, https://www.summerfoundation.org.au/

7. ‘Specialist Disability Accommodation: Position Paper on Draft Pricing and Payment (April 2016)’, NDIA, 1 April 2016, https://apo.org.au/

8. ‘NDIS Quarterly Report to disability ministers’ (2020-21 Q4), NDIS, 30 June 2021, https://www.ndis.gov.au/

This market commentary has been prepared for general informational purposes by Macquarie Asset Management Private Markets (MAM Private Markets), who are part of Macquarie Asset Management (MAM), the asset management business of Macquarie Group (Macquarie), and is not a product of the Macquarie Research Department. This market commentary reflects the views of MAM Private Markets and statements in it may differ from the views of others in MAM or of other Macquarie divisions or groups, including Macquarie Research. This market commentary has not been prepared to comply with requirements designed to promote the independence of investment research and is accordingly not subject to any prohibition on dealing ahead of the dissemination of investment research.

Nothing in this market commentary shall be construed as a solicitation to buy or sell any security or other product, or to engage in or refrain from engaging in any transaction. Macquarie conducts a global full-service, integrated investment banking, asset management, and brokerage business. Macquarie may do, and seek to do, business with any of the companies covered in this market commentary. Macquarie has investment banking and other business relationships with a significant number of companies, which may include companies that are discussed in this commentary, and may have positions in financial instruments or other financial interests in the subject matter of this market commentary. As a result, investors should be aware that Macquarie may have a conflict of interest that could affect the objectivity of this market commentary. In preparing this market commentary, we did not take into account the investment objectives, financial situation or needs of any particular client. You should not make an investment decision on the basis of this market commentary. Before making an investment decision you need to consider, with or without the assistance of an adviser, whether the investment is appropriate in light of your particular investment needs, objectives and financial circumstances.

Macquarie salespeople, traders and other professionals may provide oral or written market commentary, analysis, trading strategies or research products to Macquarie’s clients that reflect opinions which are different from or contrary to the opinions expressed in this market commentary. Macquarie’s asset management business (including MAM), principal trading desks and investing businesses may make investment decisions that are inconsistent with the views expressed in this commentary. There are risks involved in investing. The price of securities and other financial products can and does fluctuate, and an individual security or financial product may even become valueless. International investors are reminded of the additional risks inherent in international investments, such as currency fluctuations and international or local financial, market, economic, tax or regulatory conditions, which may adversely affect the value of the investment. This market commentary is based on information obtained from sources believed to be reliable, but we do not make any representation or warranty that it is accurate, complete or up to date. We accept no obligation to correct or update the information or opinions in this market commentary. Opinions, information, and data in this market commentary are as of the date indicated on the cover and subject to change without notice. No member of the Macquarie Group accepts any liability whatsoever for any direct, indirect, consequential or other loss arising from any use of this market commentary and/or further communication in relation to this market commentary. Some of the data in this market commentary may be sourced from information and materials published by government or industry bodies or agencies, however this market commentary is neither endorsed or certified by any such bodies or agencies. This market commentary does not constitute legal, tax accounting or investment advice. Recipients should independently evaluate any specific investment in consultation with their legal, tax, accounting, and investment advisors. Past performance is not indicative of future results.

This market commentary may include forward-looking statements, forecasts, estimates, projections, opinions and investment theses, which may be identified by the use of terminology such as “anticipate”, “believe”, “estimate”, “expect”, “intend”, “may”, “can”, “plan”, “will”, “would”, “should”, “seek”, “project”, “continue”, “target” and similar expressions. No representation is made or will be made that any forward-looking statements will be achieved or will prove to be correct or that any assumptions on which such statements may be based are reasonable. A number of factors could cause actual future results and operations to vary materially and adversely from the forward-looking statements. Qualitative statements regarding political, regulatory, market and economic environments and opportunities are based on the Macquarie Asset Management Private Markets (MAM Private Markets) team’s opinion, belief and judgment.

None of the entities noted in this document is an authorized deposit-taking institution for the purposes of the Banking Act 1959 (Commonwealth of Australia). The obligations of these entities do not represent deposits or other liabilities of Macquarie Bank Limited ABN 46 008 583 542 (MBL). MBL does not guarantee or otherwise provide assurance in respect of the obligations of these entities.